The complete guide to a company credit check and what most businesses miss

Running a company credit check once is like checking the weather the morning before a week-long sailing trip. Useful but not the same as watching the forecast every day. But most businesses are running them at the wrong moment, reading them the wrong way, and treating a single report as a complete picture of credit risk. This guide covers what a company credit check actually tells you, and where it stops.

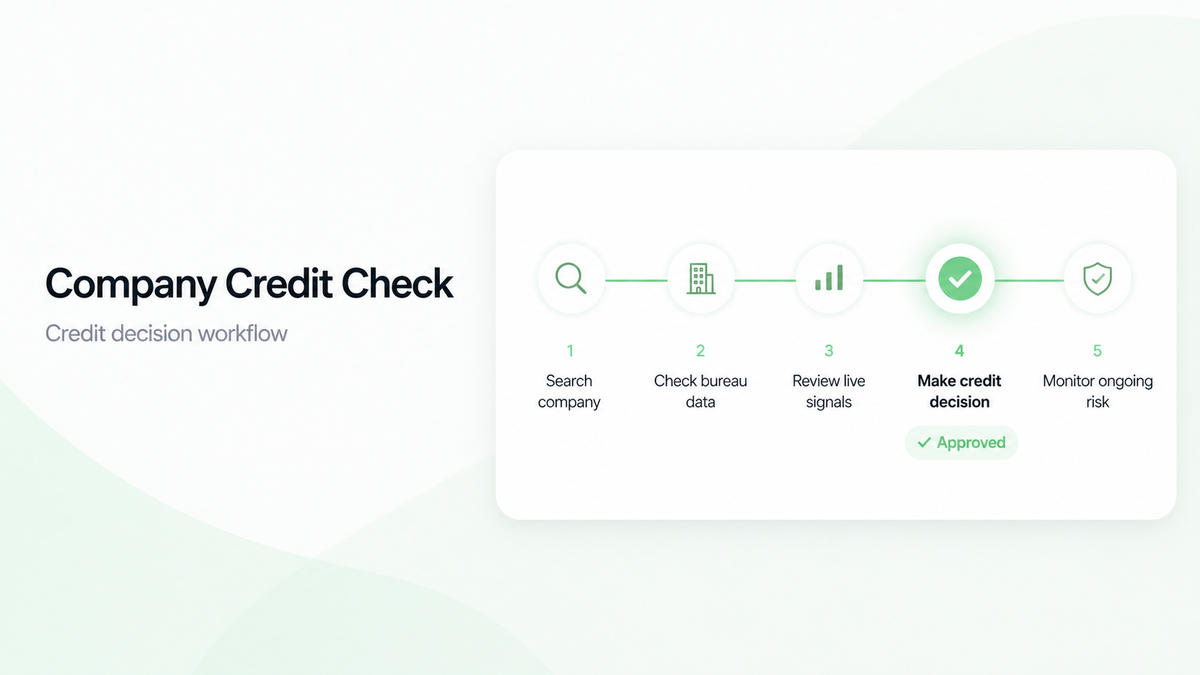

What is a company credit check?

A company credit check is an assessment of a business's financial health, creditworthiness, and risk profile. It draws on publicly filed data such as statutory accounts, county court judgements, payment history, director information, and credit scores assigned by bureau models to produce a view of how reliably a company is likely to meet its financial obligations.

Businesses run a company credit check for a range of reasons like before extending trade credit to a new customer, before taking on a significant supplier, during due diligence on a potential partner, or as part of ongoing credit risk management across an existing ledger.

Done well, a business credit check gives a credit team the confidence to say yes faster, and the intelligence to say no before exposure builds. Done poorly, or done only once, at the start of a relationship, it creates a false sense of security that can be expensive to correct.

What a company credit check typically covers

A standard business credit check will usually include some combination of the following:

- Filed statutory accounts (profit, loss, balance sheet)

- Credit score and suggested credit limit

- County court judgements (CCJs) and other legal notices

- Director history and disqualifications

- Payment performance data (where available)

- Company structure, group ownership, and charges

- Industry risk classification

This is genuinely useful information. The question is not whether a company credit check has value as it clearly does. The question is what it cannot tell you, and how much of your credit risk management depends on the answer.

The structural limits of a bureau-based company credit check

The most important thing to understand about a traditional company credit check is that it is, by design, a backwards-looking document. The statutory accounts it draws on are filed months, sometimes well over a year after the period they describe. A business that filed healthy accounts nine months ago may be in serious difficulty today. A bureau-based business credit check will not tell you that.

A company credit check run at onboarding reflects the business as it was — not as it is. For a 60-day credit relationship, that distinction matters enormously.

There are three specific gaps that credit teams relying solely on bureau reports tend to encounter:

1. No ongoing monitoring

A company credit check is a snapshot. Once it is run, the data begins ageing immediately. Most bureau-based credit risk management workflows run a check at onboarding and then rely on periodic reviews, either quarterly or annually, to catch changes. In practice, that means a business can deteriorate significantly between checks with no signal reaching the credit team.

2. No operational or reputational signals

Filed accounts capture financial outcomes. They do not capture the operational and reputational signals that often precede those outcomes: slower payments to suppliers, management instability, shrinking headcount, compliance issues, or reputational deterioration. A business credit check built solely on bureau data misses the warning signs that experienced credit professionals learn to spot in the real world.

3. Slow decisions on good customers

Ironically, the same bureau-first process that misses risk on deteriorating businesses also slows down decisions on healthy ones. When a company credit check requires manual document collection, cross-referencing, and internal sign-off, onboarding takes hours. In competitive markets, that cost is measured in lost accounts, not just staff time.

Company credit check vs. continuous credit risk management

The distinction between a company credit check and a credit risk management programme is worth making explicit, because they are often conflated.

A company credit check is a tool. A report generated at a point in time, based on available data. A credit risk management programme is a system. One that uses that tool alongside others, monitors trading partners over time, integrates into business operations, and generates decisions rather than just data.

Many businesses have the tool. Fewer have the system. The gap between the two is where bad debts live.

What to look for in a company credit check provider

Not all business credit check tools are built the same way. When evaluating providers, the questions that matter most are not about price per report. They are about what the tool can actually do for your credit risk management over the life of a trading relationship.

- Does it monitor companies continuously, or only at the point of check?

- Does it draw on multiple data sources beyond statutory filings?

- Can it integrate with your existing ERP or CRM?

- Does it surface early warning signals, not just confirmed deterioration?

- Can it support decisions at scale across a full customer ledger, not just individual queries?

And on what to look out for:

- Does it require manual effort to pull reports and track changes?

- Does it rely primarily on data that is months or years old?

- Is it a one-time snapshot with no ongoing monitoring capability?

Why Grand goes further than a standard company credit check

Grand was built for businesses in the trade economy that need more than a point-in-time company credit check. Rather than generating static reports from historical filings, Grand builds and maintains live profiles on all UK businesses, analysing thousands of financial, operational, and reputational data points continuously, so the picture a credit team sees reflects what is happening now, not what was filed last year.

That means a company credit check run through Grand is not a one-time event. It is the start of an ongoing view of every trading partner on your ledger, one that updates automatically, surfaces risk before it becomes exposure, and integrates directly into the systems your team already uses.

For businesses serious about credit risk management. Not just the onboarding checkbox, but genuine protection of revenue across the life of every relationship, that is a fundamentally different proposition to a bureau report.

Grand gives credit teams real-time visibility into company credit risk powered by early signals, continuous business behaviour, and AI foresight. If you want to see what your current tools are missing, get in touch.